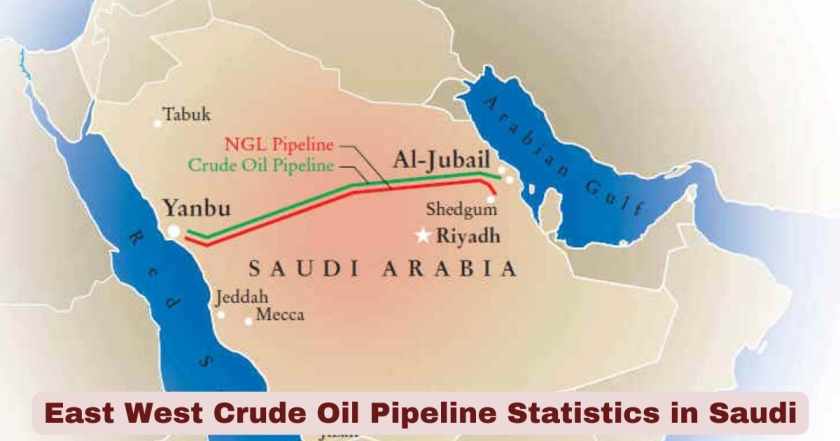

What is East West Crude Oil Pipeline in Saudi Arabia?

The East West Crude Oil Pipeline — universally known as the Petroline or the Abqaiq-Yanbu Pipeline — is Saudi Arabia’s most strategically critical piece of domestic energy infrastructure: a 1,201-kilometre (746-mile) dual-pipe system that crosses the entire width of the Arabian Peninsula from the Abqaiq oil processing complex in the Eastern Province, near the Persian Gulf coast, to the Red Sea port of Yanbu in the Hejaz region. It is the only major operational pipeline in the world that was purpose-built to allow a single country to bypass the Strait of Hormuz entirely — delivering crude oil to international export terminals on a completely separate coastline, unreachable by any naval force controlling the Strait. Its origins lie in the 1979 Iranian Revolution and the subsequent outbreak of the Iran-Iraq War in 1980, events that confronted Saudi Arabia’s leadership with a terrifying strategic vulnerability: the kingdom’s entire export income — and therefore its national survival — depended on oil passing through a narrow waterway that a hostile regional power could theoretically close. King Khalid authorised construction in 1979, the pipeline was built by Petromin (the state petroleum organisation predecessor to Aramco’s full nationalisation), and the first oil flowed in 1981 at a cost of approximately $2.5 billion — equivalent to roughly $8.5 billion in 2026 dollars. The pipeline’s original capacity of 5 million barrels per day was further expanded over decades, culminating in an emergency maximum capacity of 7 million barrels per day — achieved by converting adjacent natural gas liquids pipelines to carry crude oil, first demonstrated after the 2019 Houthi drone strikes on Abqaiq. That 7 million bpd emergency figure was never tested at sustained flows until the events of March 2026.

As of 2026, the Petroline is no longer a strategic insurance policy sitting in reserve — it is the active lifeline of Saudi Arabia’s entire export economy, operating at its maximum 7 million barrels per day capacity for the first time in its 45-year history. The trigger is the most consequential energy crisis of the modern era: the closure of the Strait of Hormuz following Iran’s decision on March 2, 2026 to formally blockade the waterway in response to Operation Epic Fury — the US-Israel military campaign launched on February 28, 2026. The Strait, which before the war carried approximately 20 million barrels per day — roughly one-fifth of all global petroleum consumption — became impassable for non-Iranian vessels almost overnight. Saudi Arabia’s exports via Ras Tanura, which totalled approximately 5.5 million bpd through the Strait before the war, were effectively shut off. In the same timeframe, Yanbu’s crude loadings surged by 330% from pre-war levels, with 27 Very Large Crude Carriers observed lined up at anchorage by maritime AI company Windward, and Saudi Aramco CEO Amin Nasser publicly stated on March 10, 2026 — on the company’s earnings call, of all forums — that the Petroline would reach full 7 million bpd capacity within days. That full capacity was achieved on March 11, 2026. The Petroline, built 45 years ago to prepare for exactly this scenario, is now being tested at exactly this scale, for the first time, in exactly the conflict environment its designers anticipated.

Interesting Facts About the East West Crude Oil Pipeline 2026

| Fact | Detail |

|---|---|

| Official Name | East–West Crude Oil Pipeline — Arabic: خط أنابيب النفط الخام الشرق-غرب |

| Common Names | Petroline (industry standard name); Abqaiq-Yanbu Pipeline; informally “the Lifeline” in 2026 media coverage |

| Owner / Operator | Saudi Aramco — wholly state-owned; originally built by Petromin (General Petroleum and Mineral Organization) |

| Pipeline Type | Dual pipeline system — one 48-inch and one 56-inch diameter steel pipe running in parallel |

| Total Length | 1,201 km (746 miles) — crosses the entire Arabian Peninsula west-northwest |

| Origin Point | Abqaiq oil processing complex, Eastern Province — the largest crude oil stabilisation facility in the world (capacity: 7 million bpd) |

| Terminus Point | King Fahd Industrial Port (KFIP), Yanbu, Red Sea — also known as Yanbu Export Terminal |

| Countries Traversed | Saudi Arabia only — entirely domestic; crosses no international borders |

| Purpose | Bypass the Strait of Hormuz — deliver Saudi crude to Red Sea for export to Europe, Asia, US without transit through Persian Gulf or Strait |

| Strategic Vision | “Built with this in mind for contingency” — Aramco CEO Amin Nasser, March 10, 2026 |

| Authorising Monarch | King Khalid bin Abdulaziz — authorised construction 1979 |

| Construction Year | 1979–1981 (completed and first oil flowing 1981) |

| Original Construction Cost | ~$2.5 billion (~$8.5 billion in 2026 dollars) |

| Original Builder | Petromin (state organisation); Aramco constructed parallel NGL pipeline simultaneously |

| Original Capacity (1981) | ~5 million barrels per day (bpd) — initial design capacity |

| Capacity (1992) | 5 million bpd — confirmed; 56-inch line operating at 2 million bpd while 48-inch handled NGL |

| Capacity (2018) | 5 million bpd — operational norm under dual crude-carrying configuration |

| Capacity (March 2025 — Aramco announcement) | 7 million bpd — Aramco reported expanded capacity; not yet tested at sustained flows (IEA) |

| Capacity (March 11, 2026) | 7 million bpd — fully activated for first time; NGL pipelines converted to crude; Strait of Hormuz crisis |

| Pumping Stations | 13 pumping stations — Knowledge Base (March 12, 2026); GEM Wiki: 11 pumping stations + 2 break stations |

| Turbines Along the Line | 65 gas turbines — power the pump stations (the 48-inch line also supplies gas to these turbines) |

| Pre-War Normal Throughput | ~1 million – 2.8 million bpd — Nasser: “somewhere in the neighbourhood of about 2.8 million bpd” before war; Jim Bianco Research: ~1 million bpd |

| Crude Oil Supplied to Yanbu Refineries | ~2 million bpd — fed to Aramco’s and Yanbu National Petrochemical Co. refineries before export headroom available |

| Pre-War Export Capacity from Yanbu | ~760,000 bpd — Kpler data (Argus Media, March 2026) |

| Normal Export via Hormuz (pre-war) | 5.5 million bpd — Saudi crude and condensate via Ras Tanura and Ju’aymah (Kpler, EIA) |

| Saudi Arabia Crude Production (2025) | 9.48 million bpd — Argus Media / Kpler |

| Saudi Arabia Crude Exports (2025) | 6.3 million bpd crude + 1.4 million bpd refined products — Kpler |

| Saudi Arabia Maximum Sustainable Capacity | 12.2 million bpd — Aramco official figure |

| 2019 Houthi Drone Attack | 14 May 2019 — Petroline attacked by Houthi drones; two pumping stations hit near Dawadmi and Al-Afif; operations briefly suspended but quickly restored |

| IPSA Pipeline (parallel) | Iraqi Pipeline in Saudi Arabia — 1.65 million bpd capacity, 48-inch; runs parallel from Pump Station No. 3 to Al-Mu’ajjiz port south of Yanbu; out of operation since Desert Storm (1991); potential emergency revival discussed in 2026 |

Source: Wikipedia (East–West Crude Oil Pipeline, updated March 14, 2026), IEA Strait of Hormuz report (2026), US EIA (June 2025 and March 2026), Global Energy Monitor (GEM.wiki, March 3, 2026), S&P Global Commodities (March 10, 2026), Lloyd’s List (March 9, 2026), Argus Media (March 10, 2026), OilPrice.com (March 11, 2026), Knowledge Base (March 12, 2026), House of Saud (March 12–13, 2026), Engineering News-Record (March 12, 2026), Asharq Al-Awsat (March 2026), Jim Bianco Research/X (March 2026)

The historical context of the Petroline’s creation is inseparable from Iran’s direct role in its conception and now its maximum operational activation. The same Iranian Revolution of 1979 that stripped the Shah from power and triggered Saudi Arabia’s decision to build this pipeline is the same geopolitical force — now in the form of Iran’s military campaign to close the Strait of Hormuz — that has brought the pipeline to its first-ever full operational test 45 years later. Saudi Arabia’s strategic planners of the late 1970s made a bet that proved correct: that building a second export route, however expensive, was worth paying for. The cost of the original construction at $2.5 billion (1981 dollars) is trivially small compared to the billions of dollars of export revenue now flowing through the pipeline every week that would otherwise be lost if the Strait closure had found Saudi Arabia without an alternative. The pipeline is not just infrastructure — it is a 45-year-old strategic wager that has paid off at exactly the moment it was supposed to.

The dual pipeline architecture — one 48-inch and one 56-inch line — was not an overengineering decision but a deliberate redundancy choice. The 56-inch line carries crude; the 48-inch line was originally designed to carry both crude and to supply gas to the 65 turbines powering the pump stations along the route. Converting the 48-inch line from gas/NGL service to full crude carrying capacity — which is the mechanism through which the system reaches 7 million bpd — was first demonstrated under pressure in 2019 after the Houthi drone attack on Abqaiq. That exercise, while involuntary, proved that Aramco’s engineers could execute the conversion in days rather than weeks and that the pipeline’s structural integrity under maximum throughput was sound. The 2026 activation is, in engineering terms, the same operation done at greater urgency, greater duration, and with the entire global oil market watching every barrel.

East West Pipeline Technical & Infrastructure Statistics 2026

| Metric | Data |

|---|---|

| Pipeline 1 Diameter | 48 inches (122 cm) |

| Pipeline 2 Diameter | 56 inches (142 cm) |

| Pipeline 1 Primary Role | Originally: natural gas liquids (NGL) + gas supply to pump station turbines; now: converted to carry crude oil in emergency max-capacity mode |

| Pipeline 2 Primary Role | Crude oil transport — always the primary crude line |

| Total Pipeline Length | 1,201 km (746 miles) across the Arabian Peninsula |

| Pipe Material | High-grade steel — built to withstand desert temperature extremes; anticorrosion coating |

| Route Terrain | Flat Eastern Province desert → Dahna sand sea → central Arabian plateau → Hejaz mountain escarpment → coastal plain → Yanbu |

| Maximum Elevation Crossed | Hejaz Mountains — requires pumping pressure to push crude over escarpment before gravity-assisted descent to coast |

| Number of Pumping Stations | 13 — Knowledge Base (March 2026); GEM: 11 pump + 2 break stations |

| Gas Turbines at Pump Stations | 65 gas turbines — power all pumping operations; fuelled by pipeline gas |

| Pump Station 3 Location | Strategic junction where IPSA (Iraqi Pipeline in Saudi Arabia) intersects — 225 km from Abqaiq |

| Origin Facility: Abqaiq | World’s largest crude oil stabilisation plant — processes raw crude from Ghawar, Safaniyah, and Shaybah fields; capacity 7 million bpd |

| Key Oilfields Connected to Abqaiq | Ghawar (world’s largest conventional oilfield), Safaniyah (world’s largest offshore field), Shaybah, Hawiyah, Haradh |

| Destination: King Fahd Industrial Port | Yanbu, Red Sea — also served by parallel Abqaiq-Yanbu NGL pipeline (capacity 300,000 bpd; fully utilised separately) |

| Abqaiq-Yanbu NGL Pipeline | Runs parallel to Petroline — 300,000 bpd capacity; carries natural gas liquids separately from crude |

| Domestic Refineries Served (Yanbu) | Yanbu National Petrochemical Company (YANSAB) + Saudi Aramco Yanbu Refinery — together receive ~2 million bpd |

| Normal Crude Reserved for Refineries | ~2 million bpd — fed to Yanbu industrial zone before any export headroom is available |

| Maximum Export Headroom (pipeline alone) | 7 million bpd total − 2 million bpd refinery = 5 million bpd available for export |

| 2014 Configuration | 56-inch line operating at 2 million bpd; 48-inch line converted from NGL to crude — combined 5 million bpd from that point |

| 2016 Expansion Plan | Aramco planned 5 → 7 million bpd expansion by 2018 — a 40% capacity increase — Pipeline Technology Journal, June 2016 |

| 2019 Emergency Activation | After Houthi attack on Abqaiq (September 2019): NGL lines converted; 7 million bpd demonstrated for first time |

| March 2025 Aramco Report | Aramco confirmed 7 million bpd capacity in formal report — not yet tested at sustained flows — IEA |

| IEA Spare Capacity Assessment (early 2026) | ~2 million bpd actually used out of 7 million bpd capacity — IEA estimated 3–5 million bpd spare capacity available |

| IPSA Capacity (dormant) | 1.65 million bpd — parallel 48-inch pipeline from Pump Station 3 to Al-Mu’ajjiz; out of service since 1991 |

| IPSA Revival Feasibility (2026) | 2–3 months rehabilitation needed; 500,000–800,000 bpd could be restored in 6–12 months — House of Saud analysis |

| Pipeline Operating Pressure | High — sufficient to push crude over Hejaz escarpment; maintained by 13 pump stations |

| Pigging / Maintenance | Regular pipeline inspection and cleaning via intelligent pigs (inspection devices run through the pipe) |

Source: Wikipedia (updated March 14, 2026), GEM.wiki (March 3, 2026), Knowledge Base (March 12, 2026), IEA Strait of Hormuz (2026), US EIA, House of Saud (March 12–13, 2026), Engineering News-Record (March 12, 2026), Global Energy Monitor, Baker Institute (IPSA paper)

The technical infrastructure statistics reveal a pipeline system that is simultaneously simpler in conception and more complex in execution than most major energy installations of comparable strategic importance. The gravity of the challenge posed by the Hejaz mountain escarpment — where the pipeline must push crude uphill across a mountain range before it can descend to the Red Sea — required careful pump station placement along the route, with the pressure management ensuring consistent flow rates despite the changing elevation profile. The 65 gas turbines powering the pump stations are an integrated system: the gas that fuels them was historically partly sourced from the same 48-inch pipeline that also carried NGL — which is precisely why converting that line to crude requires simultaneously arranging alternative gas supply for the pump station turbines, a logistical complexity that is invisible in the headline capacity figures but critical to actual operations.

The Abqaiq processing complex’s 7 million bpd processing capacity — matching exactly the Petroline’s maximum throughput — is not a coincidence but a deliberate design alignment: there is no value in a pipeline that can move more crude than the processing facility at its head can prepare for transport. The worlds’ largest crude stabilisation plant, Abqaiq, removes volatile gases from raw crude to make it safe and stable for pipeline and tanker transport. The three oilfields that feed it — Ghawar, the largest conventional oilfield on earth; Safaniyah, the largest offshore field in the world; and Shaybah in the Empty Quarter — form the reservoir base for most of the crude flowing through the Petroline. When the pipeline operates at 7 million bpd, Abqaiq is simultaneously processing at its own ceiling — a system-wide synchronisation that has never been sustained at this level for more than days at a time before March 2026.

East West Pipeline Yanbu Terminal Statistics 2026

| Metric | Data |

|---|---|

| Terminal Name | King Fahd Industrial Port (KFIP), Yanbu — Saudi Arabia’s primary Red Sea crude export terminal |

| Location | Yanbu al-Sinaiyah (Yanbu Industrial City), Madinah Province, Red Sea coast — coordinates: ~24.08°N, 38.05°E |

| Distance from Abqaiq | ~1,201 km (746 miles) via pipeline |

| Terminal Sub-Facilities | Yanbu North Terminal (older) + Yanbu South Terminal (added 2018) |

| Yanbu North Loading Capacity | ~1.5 million bpd — Argus Media |

| Yanbu South Loading Capacity | ~3 million bpd — Argus Media |

| Nominal Combined Loading Capacity | ~4.5 million bpd — Argus Media / ENR (March 2026) |

| Effective / Operationally Tested Capacity | ~4 million bpd — market sources consensus (ENR, Argus) |

| Vortexa Wartime Capacity Estimate | ~3 million bpd — under current wartime operational conditions |

| Pre-War Yanbu Crude Exports (2025) | ~760,000 bpd — Kpler annual average (Argus Media) |

| Pre-War Yanbu Crude Exports (Feb 2026) | ~800,000 bpd — Nasser reference point |

| Post-War Yanbu Loadings (Mar 2–8, 2026) | 2.72 million bpd — Vortexa (Lloyd’s List, March 9, 2026) |

| Post-War Yanbu Loadings (Mar 10, 2026) | 2.2–2.47 million bpd — Kpler (Argus) / Windward |

| Surge vs Pre-War Level | ~330% increase — Windward Maritime AI |

| Alternative Ports Loading (Mar 2–8, 2026) | 6.52 million bpd total from all alternative ports (Yanbu + Fujairah + Muscat) — Vortexa |

| Alternative Ports Surge vs Jan 2023 Average | ~90% higher than 3.44 million bpd average observed since January 2023 |

| Yanbu’s Share of Alternative Port Loadings | 42% — Vortexa (March 2–8, 2026) |

| Supertankers at Yanbu Anchorage (March 2026) | 27 VLCCs observed heading to Yanbu — Windward (OilPrice.com) |

| VLCCs at Anchor (Jim Bianco, March 2026) | 18 red dots (anchored tankers) visible on Marine Traffic real-time map at Yanbu |

| Post-War Yanbu Cargo Loadings | 1.9 cargoes loaded per day = ~372,000 tonnes/day = 1.24 VLCCs/day (at 300,000 DWT) — Vortexa |

| At 5 Million bpd Export Rate | 2.27 VLCCs/day could be loaded — Vortexa projection |

| 5 Supertankers Already Departed (early Mar) | ~10 million barrels loaded and departed westward in first days of ramp-up |

| Aramco Strategy | Requesting Asian buyers to nominate April crude loading plans for both Ras Tanura and Yanbu — OilPrice.com |

| Crude Grade Exported via Yanbu | Primarily Arab Light — the 56-inch pipeline’s standard throughput grade |

| Normal Yanbu Export Premium | ~$0.25/barrel above Ras Tanura (pipeline cost premium) — Baker Institute reference |

| Bottleneck Issue | Pipeline can move 7 million bpd; Yanbu terminals can load only ~4–4.5 million bpd; ~2 million bpd fed to local refineries = effective net export cap ~2–2.5 million bpd at present operational tempo |

| SUMED Pipeline (Egypt) Connection | Some Yanbu crude historically directed to SUMED pipeline (Ain Sukhna to Sidi Kerir) for Mediterranean market access — an additional Red Sea routing option |

Source: Argus Media (March 10, 2026), Lloyd’s List (March 9, 2026), OilPrice.com (March 11, 2026), Vortexa (via Lloyd’s List and OilPrice.com), Windward Maritime AI (OilPrice.com), Kpler (via Argus Media), ENR (March 12, 2026), S&P Global (March 10, 2026), Jim Bianco Research/X (March 2026), House of Saud (March 12, 2026)

The Yanbu terminal statistics lay bare the most fundamental structural problem in Saudi Arabia’s Hormuz bypass strategy: the pipeline can move more oil than the terminal can load. At 7 million bpd flowing through the pipe, minus 2 million bpd consumed by Yanbu’s refineries, there are 5 million bpd of crude looking for tankers to load — but Yanbu’s combined terminal capacity of 4–4.5 million bpd creates a ceiling that even maximum pipeline flow cannot break through. And the “effective” capacity under wartime surge conditions — with more simultaneous vessel movements, anchor congestion, pilot shortages, and berth scheduling conflicts — may be even lower, with Vortexa estimating just 3 million bpd of practical loading capacity. The physical constraint is not the pipe; it is the berths, loading arms, manifolds, and metering systems at the Yanbu North and South terminals, which were sized for the pipeline’s normal 1–2 million bpd throughput level and were never upgraded to match the pipeline’s theoretical 7 million bpd ceiling.

The 330% surge in Yanbu loadings measured by Windward Maritime AI — from approximately 760,000 bpd in February to 2.47 million bpd in the first week of March 2026 — is the real-world stress test that demonstrates both the pipeline’s genuine responsiveness and the terminal’s genuine ceiling simultaneously. The image of 27 VLCCs converging on Yanbu — each carrying approximately 2 million barrels — and 18 supertankers sitting at anchor waiting for berths while five others depart loaded, is the definitive visual metaphor for the situation: enormous latent supply, constrained by the final loading interface. The solution that Saudi Arabia and Aramco are pursuing — dual-port loading at both Yanbu and Jeddah, and potentially rehabilitation of the IPSA pipeline to Al-Mu’ajjiz for additional Red Sea loading points — reflects exactly the infrastructure calculus that the original pipeline designers accepted as a limitation: build the pipe, and accept that full export capacity would require port expansion investment that the pre-crisis economics never justified.

East West Pipeline Strategic & Economic Statistics 2026

| Metric | Data |

|---|---|

| Strait of Hormuz Pre-War Daily Flow | ~20 million bpd — crude, condensate, and oil products — IEA / US EIA (2025 average) |

| Hormuz LNG Flow (2025) | Over 112 bcm — Qatar and UAE LNG; ~20% of global LNG trade |

| Saudi Crude via Hormuz (2024) | 5.5 million bpd — 38% of total Hormuz crude flows — US EIA |

| Total Hormuz Crude Flows (2024) | ~14.5 million bpd crude and condensate |

| Petroline Bypass Capacity vs Hormuz Flow | Maximum 5 million bpd exportable via Yanbu vs ~20 million bpd that transited Hormuz — covers only 25% of Hormuz volume |

| Saudi + UAE Combined Bypass Capacity | 3.5–5.5 million bpd — IEA estimate; Saudi Petroline 5M + UAE ADCOP 1.8M |

| Pre-War Saudi Export via Ras Tanura | ~5.5 million bpd (Hormuz route) — effectively shut off March 2, 2026 |

| Ras Tanura + Ju’aymah Combined Loading Capacity | 6.5 million bpd — lost to Hormuz closure (House of Saud) |

| Revenue Lost per Day (Saudi, if no Petroline) | At $100/barrel: 5.5 million bpd × $100 = $550 million/day — entirely dependent on Petroline to recover any portion |

| Brent Crude Price (March 10, 2026) | ~$100/barrel — Asharq Al-Awsat |

| Barclays Price Forecast (if Hormuz stays closed 4–6 weeks) | $100/barrel average for 2026 — Barclays, Argus Media |

| Barclays Baseline (Hormuz reopens in 2–3 weeks) | $85/barrel average for 2026 |

| IEA Description of Disruption | “The largest [oil disruption] in history” — International Energy Agency (Knowledge Base, March 12, 2026) |

| Aramco Net Income (Full Year 2025) | $93.4 billion — down 12% year-over-year (lower revenues + other income) |

| Aramco Q4 2025 Net Income Drop | Down ~24% quarter-on-quarter — higher operating costs |

| Aramco Capex 2025 | $52.2 billion — in line with guidance; $1 billion lower year-on-year |

| Aramco Capex Guidance 2026 | $50–55 billion |

| Amin Nasser Assessment | “The biggest crisis the region’s oil and gas industry has faced” — Aramco CEO, March 10, 2026 |

| Aramco Storage Offshore | Has storage facilities in Japan, South Korea, Netherlands, Mediterranean — tapping to “meet majority of customers’ requirements” |

| Storage Adequacy Warning | Nasser: adequate inventories only “provided [the war] does not persist in the long term” |

| Saudi Arabia Percentage of Global Oil | ~10% of global oil production — one of the three largest producers globally |

| European Distillate Crisis | ~30% of Europe’s diesel and 50% of jet fuel came from Middle East pre-war — Argus/Global Risk Management |

| Arne Lohmann Rasmussen Quote | “This is very much a distillate crisis. A jet fuel and diesel crisis, especially in Europe.” — Chief Analyst, Global Risk Management, Middle East Eye |

| Ellen Wald on Petroline Trade-off | “Maximizing Petroline’s crude throughput means abandoning its role carrying natural gas liquids and products” — Transversal Consulting founder, ENR |

| Russia’s War Benefit | OilPrice.com: Russia emerges as biggest winner — Russian oil outside Hormuz, priced at a premium due to scarcity |

| ADCOP (UAE parallel pipeline) | Abu Dhabi Crude Oil Pipeline — 1.8 million bpd; Habshan to Fujairah (Gulf of Oman); cost $4.2 billion; operational since June 2012 |

Source: IEA Strait of Hormuz report (2026), US EIA (June 2025 / March 2026), Argus Media (March 10, 2026), S&P Global (March 10, 2026), ENR (March 12, 2026), Knowledge Base (March 12, 2026), OilPrice.com (March 11, 2026), Asharq Al-Awsat (March 2026), House of Saud (March 12–13, 2026), Barclays (via Argus Media), Global Risk Management / Middle East Eye

The strategic and economic statistics for the East West Pipeline in March 2026 frame a scenario of extraordinary financial and geopolitical consequence. Saudi Arabia’s export position before the war — 6.3 million bpd of crude and 1.4 million bpd of refined products — generated, at Brent prices of $80–100/barrel, a gross export revenue stream of approximately $200–250 million per day from crude alone. The closure of Ras Tanura — which handled approximately 5.5 million bpd of that export volume — did not eliminate Saudi export revenue but compressed it dramatically: Yanbu can load approximately 2–2.5 million bpd net of refinery supply, at a time when the pipeline is flowing at 7 million bpd. The remaining 4.5–5 million bpd either accumulates in storage (which is finite) or forces production curtailment — losing revenue that cannot be recovered after the crisis ends. The Petroline is not solving the problem; it is buying time while Saudi Arabia and its allies work toward Strait reopening.

The “distillate crisis” identified by Arne Lohmann Rasmussen of Global Risk Management — where the closure affects not just crude oil but jet fuel, diesel, and naphtha that cannot travel through any bypass pipeline — reveals the deepest structural limitation of the Petroline as a crisis tool. The pipeline carries crude oil only. The Yanbu terminals export crude oil to refiners around the world. But the product tankers that carried 5 million bpd of refined diesel, jet fuel, naphtha, and LPG through the Strait have no pipeline alternative — those products can only leave the Gulf by sea. Europe’s dependence on Middle Eastern jet fuel and diesel — roughly 30% of diesel and 50% of jet fuel by Rasmussen’s estimate — cannot be addressed by the Petroline at all. This is the structural gap that Saudi Arabia’s infrastructure investment, impressive as it is, cannot bridge: the bypass was designed for crude, and the world now needs a bypass for everything.

East West Pipeline Iran War Activation Statistics 2026

| Metric | Data |

|---|---|

| Operation Epic Fury Start Date | February 28, 2026 — US-Israel war against Iran; joint strikes on military, nuclear, government infrastructure |

| Strait of Hormuz Formal Closure | March 2, 2026 — Iranian IRGC formally declared Strait closed; attacks on non-Iranian tanker traffic commenced |

| Strait Closure Pre-War Traffic | ~20 million bpd petroleum liquids — roughly one-fifth of global consumption |

| Saudi Hormuz Exports Shut Off | ~5.5 million bpd via Ras Tanura — effectively offline from March 2, 2026 |

| Petroline Throughput (Pre-War, Nasser) | ~2.8 million bpd — normal operational rate before February 28, 2026 |

| Petroline Throughput (Jim Bianco, pre-war) | ~1 million bpd — lower estimate of normal use |

| IEA Estimate (Early 2026) | ~2 million bpd actually flowing; 3–5 million bpd spare capacity available |

| Aramco Ramp-Up Decision | “Immediately as the ports were starting to close, we ramped up production through the East-West Pipeline” — Amin Nasser, Lloyd’s List investor call |

| CEO Public Announcement Date | March 10, 2026 — Aramco’s Q4 2025 / FY 2025 earnings call |

| CEO Statement | “The 7 million b/d East-West pipeline connecting Saudi Arabia’s eastern and western coasts will hit full capacity ‘in the next couple of days'” — S&P Global, March 10 |

| Full 7 Million bpd Capacity Achieved | March 11, 2026 — per Wikipedia (updated March 14, 2026); IEA Strait of Hormuz reference |

| First Time Ever at Full Capacity | Yes — 7 million bpd had never been sustained before; Hormuz crisis is the first real test |

| Yanbu Loading Rate (Mar 2–8 vs pre-war) | From ~760,000 bpd (2025 annual average) → 2.72 million bpd (week of Mar 2–8) |

| Yanbu Loading Surge | +330% from pre-war levels — Windward Maritime AI |

| Alternative Port Loadings (Mar 2–8) | 6.52 million bpd total — Yanbu (2.72M) + Fujairah (1.9M) + Muscat (1.25M) + others — Vortexa |

| VLCCs at Yanbu (Windward observation) | 27 supertankers observed heading to Yanbu — OilPrice.com March 11, 2026 |

| 5 Supertankers Departed Loaded | ~10 million barrels already shipped westward in first days — S&P Global |

| Aramco Storage Drawdown | Activating Japan, South Korea, Netherlands, Mediterranean storage to bridge supply gaps |

| Yanbu + Jeddah Dual-Port Loading | Strategy to supplement Yanbu loadings using Jeddah Commercial Port capacity for additional uplift |

| Saudi Pre-War Export via Ras Tanura | ~5.5 million bpd — cannot be replicated by Yanbu alone |

| Net Export Gap | Even at max pipeline flow: Yanbu can export ~2–2.5M bpd net → shortfall of ~3M bpd vs pre-war levels |

| Trump Naval Escort Proposal | Trump called for allied navies to escort tankers through Hormuz; Nasser said Aramco sells Free On Board (FOB) — buyer’s responsibility for shipping |

| Black Sea Grain Deal Parallel | UK/EU officials discussed a UN-brokered initiative modelled on the Ukraine Black Sea Grain Corridor — to restore Hormuz tanker passage |

| Keir Starmer UK Statement | “We will not be drawn into the wider war. We’re working with allies to bring together a viable, collective plan to restore freedom of navigation.” — March 10, 2026 |

| Barclays Crude Price Forecast | If Hormuz closed 4–6 weeks: Brent averages $100/barrel for 2026; if normalised in 2–3 weeks: $85/barrel |

| Nasser Long-Term Warning | Storage adequate only “provided [the war] does not persist in the long term” |

Source: Wikipedia (East–West Crude Oil Pipeline, March 14, 2026), S&P Global (March 10, 2026), Lloyd’s List (March 9, 2026), Argus Media (March 10, 2026), IEA Strait of Hormuz (2026), OilPrice.com (March 11, 2026), Windward Maritime AI (via OilPrice.com), Vortexa (via Lloyd’s List and Argus), Kpler (via Argus), Jim Bianco Research/X, Barclays (via Argus), ENR (March 12, 2026), Knowledge Base (March 12, 2026)

The Iran war activation statistics for the East West Pipeline document an event that Saudi Arabia’s strategic planners prepared for across four decades but hoped would never actually arrive. The pipeline was always described internally as a “contingency” — the word used by Amin Nasser himself on the March 10 investor call: “we built it with this in mind for contingency.” The speed of the ramp-up is remarkable: from approximately 2.8 million bpd pre-war to 7 million bpd within roughly two weeks of the Strait closure — a more than doubling of throughput achieved by converting NGL lines, coordinating pumping station operations across 1,201 km, and simultaneously managing the surge in tanker arrivals at Yanbu. This is the operational competence that Aramco’s 2019 Abqaiq response demonstrated — and that the 2026 crisis has confirmed at an order of magnitude greater scale.

The structural incompleteness of the Petroline solution — that it can move 7 million bpd but Yanbu can only load 4 million bpd effectively, of which 2 million bpd feeds local refineries, leaving only ~2 million bpd of net export flow — means the pipeline addresses approximately one-third of the problem created by Hormuz closure. The remaining two-thirds of lost export volume must be bridged by offshore storage drawdowns (finite), production curtailment (permanent revenue loss), and ultimately Strait reopening (dependent on geopolitical resolution). Amin Nasser’s quiet admission that storage reserves are adequate only “provided [the war] does not persist in the long term” is the most consequential energy security statement made by any CEO in 2026 — and the reason why the East West Crude Oil Pipeline, its limitations fully exposed, is simultaneously the most celebrated and most sobering piece of energy infrastructure in the world.